Batch EM in practice#

Fitting a normal variance-mean mixture is a missing-data problem: the subordinator \(Y\) is latent. The EM algorithm alternates

E-step — given the current model, compute the conditional expectations \(\mathbb{E}[t(Y) \mid X]\) of the sufficient statistics, and

M-step — set the new expectation parameters \(\eta\) to those conditional means and convert \(\eta \mapsto \theta\) via

from_expectation.

BatchEMFitter runs this loop over the full dataset each iteration. This

tutorial covers its diagnostics, regularizations, and backend options.

import jax

jax.config.update("jax_enable_x64", True)

import jax.numpy as jnp

import numpy as np

from normix import NormalInverseGaussian

from normix.fitting.em import BatchEMFitter

from normix.utils.plotting import set_theme

set_theme()

np.set_printoptions(precision=4, suppress=True)

Data and a fitter#

We simulate from a known 3-D NIG model and fit it back. BatchEMFitter.fit

returns an EMResult:

true = NormalInverseGaussian.from_classical(

mu=jnp.array([0.0, 0.0, 0.0]),

gamma=jnp.array([0.4, -0.3, 0.1]),

sigma=jnp.array([[1.0, 0.3, 0.1], [0.3, 1.0, 0.2], [0.1, 0.2, 1.0]]),

mu_ig=1.0, lam=1.5)

X = true.rvs(5000, seed=0)

init = NormalInverseGaussian.default_init(X)

fitter = BatchEMFitter(

max_iter=150, tol=1e-4, verbose=1,

e_step_backend="cpu", m_step_backend="cpu", m_step_method="newton")

result = fitter.fit(init, X)

print("converged :", result.converged)

print("iterations:", result.n_iter)

print("elapsed : %.2fs" % result.elapsed_time)

============================================================

EM Fitting: NormalInverseGaussian

============================================================

Algorithm : EM

Loop : Python loop

E-step : cpu

M-step : cpu / newton

Regularize : none

Tolerance : 1.0e-04

Max iters : 150

Converged after 31 iterations (10.92s), final LL=-4.129249

converged : True

iterations: 31

elapsed : 10.92s

The EMResult is a frozen record:

print("fields:", [f for f in result.__dataclass_fields__])

print("fitted γ:", np.asarray(result.model.gamma))

print("true γ:", np.asarray(true.gamma))

fields: ['model', 'log_likelihoods', 'param_changes', 'n_iter', 'converged', 'elapsed_time', 'diverged']

fitted γ: [ 0.4157 -0.3382 0.0818]

true γ: [ 0.4 -0.3 0.1]

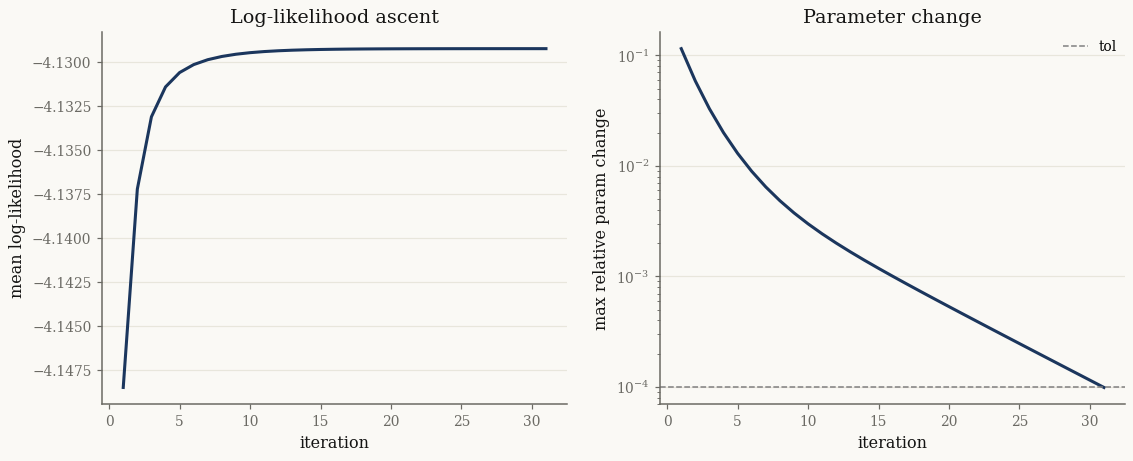

Convergence diagnostics#

With verbose >= 1 the result carries the per-iteration log-likelihood history

and the maximum relative parameter change. Both should improve monotonically and

flatten at convergence:

import matplotlib.pyplot as plt

ll = np.asarray(result.log_likelihoods)

pc = np.asarray(result.param_changes)

fig, (a0, a1) = plt.subplots(1, 2, figsize=(12, 4.4))

a0.plot(np.arange(1, len(ll) + 1), ll)

a0.set_xlabel("iteration"); a0.set_ylabel("mean log-likelihood")

a0.set_title("Log-likelihood ascent")

a1.semilogy(np.arange(1, len(pc) + 1), pc)

a1.axhline(fitter.tol, color="0.5", ls="--", lw=1, label="tol")

a1.set_xlabel("iteration"); a1.set_ylabel("max relative param change")

a1.set_title("Parameter change"); a1.legend()

plt.show()

EM never decreases the likelihood — a useful invariant when debugging a fit.

Regularizations#

Mixtures are only identified up to a scale split between \(\Sigma\) and the

subordinator. BatchEMFitter accepts a regularization to pin that gauge:

Value |

Constraint |

|---|---|

|

unconstrained |

|

\(\lvert\Sigma\rvert = 1\) |

|

\(\lvert\Sigma\rvert = \lvert\Sigma_0\rvert\) (initial value) |

|

GIG subordinator with \(a = b\) |

With det_sigma_one the fitted scale matrix has unit determinant (check

model.sigma(), the scale \(\Sigma\), not the marginal covariance):

fitter_reg = BatchEMFitter(

max_iter=150, tol=1e-4, regularization="det_sigma_one",

e_step_backend="cpu", m_step_backend="cpu")

res_reg = fitter_reg.fit(init, X)

print("det Σ (regularized):", float(jnp.linalg.det(res_reg.model.sigma())))

print("log|Σ| :", float(res_reg.model.log_det_sigma()))

det Σ (regularized): 0.9999999999999999

log|Σ| : -3.2526065174565133e-16

CPU and JAX backends#

The E-step is dominated by Bessel evaluations and the M-step by the \(\eta \mapsto \theta\) solve. Each can run on a JAX or a CPU/scipy backend independently:

e_step_backend="cpu"routes Bessel throughscipy.special.kve— a large speedup for the GIG/NIG E-step on CPU.m_step_backend="cpu"uses the numpy/scipy Newton solver for the subordinator update;m_step_methodselects"newton","lbfgs", or"bfgs".

Backends change how the arithmetic runs, not the answer:

res_jax = BatchEMFitter(

max_iter=150, tol=1e-4,

e_step_backend="jax", m_step_backend="cpu").fit(init, X)

mll_cpu = float(result.model.marginal_log_likelihood(X))

mll_jax = float(res_jax.model.marginal_log_likelihood(X))

print(f"mean log-lik (cpu E-step): {mll_cpu:.6f}")

print(f"mean log-lik (jax E-step): {mll_jax:.6f}")

mean log-lik (cpu E-step): -4.129249

mean log-lik (jax E-step): -4.129249

The convenience wrapper#

model.fit(X, ...) is a thin wrapper that builds a BatchEMFitter with the

same keywords and calls fitter.fit(self, X) — convenient for one-off fits.

Reach for BatchEMFitter directly when you need an eta_update rule (see

Incremental (mini-batch) EM) or want to reuse a configured fitter.

result2 = init.fit(X, max_iter=150, tol=1e-4, e_step_backend="cpu")

print("same fit:", bool(jnp.allclose(result2.model.gamma, result.model.gamma, atol=1e-4)))

same fit: True

Takeaways#

EM alternates an E-step (conditional moments \(\mathbb{E}[t(Y) \mid X]\)) with an M-step (

from_expectation);BatchEMFitter.fitreturns anEMResult.verbose >= 1records the log-likelihood and parameter-change histories for diagnostics; the likelihood ascends monotonically.regularizationfixes the scale gauge;e_step_backend/m_step_backend/m_step_methodtune performance without changing the optimum.

Next: Incremental (mini-batch) EM replaces the full-data sweep with mini-batches and stochastic \(\eta\)-update rules.