Normal variance-mean mixtures#

The four named mixtures — VarianceGamma, NormalInverseGamma,

NormalInverseGaussian, and GeneralizedHyperbolic — share one structure and

one API. Each has a marginal layer (the distribution of \(X\), what you

usually interact with) and a joint layer (the pair \((X, Y)\) with the latent

subordinator, used by the EM E-step). This tutorial exercises both layers.

import jax

jax.config.update("jax_enable_x64", True)

import jax.numpy as jnp

import numpy as np

from normix import (

VarianceGamma, NormalInverseGamma,

NormalInverseGaussian, GeneralizedHyperbolic,

)

from normix.utils.plotting import set_theme

set_theme()

np.set_printoptions(precision=4, suppress=True)

A common constructor#

All four marginals build from the location \(\mu\), the skewness vector \(\gamma\), a covariance \(\Sigma\), and the subordinator’s own parameters:

mu = jnp.array([0.0, 0.0])

gamma = jnp.array([0.3, -0.4])

Sigma = jnp.array([[1.0, 0.3], [0.3, 1.0]])

models = {

"VarianceGamma": VarianceGamma.from_classical(

mu=mu, gamma=gamma, sigma=Sigma, alpha=1.5, beta=1.5),

"NormalInverseGamma": NormalInverseGamma.from_classical(

mu=mu, gamma=gamma, sigma=Sigma, alpha=3.0, beta=2.0),

"NormalInverseGaussian": NormalInverseGaussian.from_classical(

mu=mu, gamma=gamma, sigma=Sigma, mu_ig=1.0, lam=1.5),

"GeneralizedHyperbolic": GeneralizedHyperbolic.from_classical(

mu=mu, gamma=gamma, sigma=Sigma, p=-0.5, a=1.0, b=1.0),

}

for name, m in models.items():

print(f"{name:24s} mean={np.asarray(m.mean())} d={m.d}")

VarianceGamma mean=[ 0.3 -0.4] d=2

NormalInverseGamma mean=[ 0.3 -0.4] d=2

NormalInverseGaussian mean=[ 0.3 -0.4] d=2

GeneralizedHyperbolic mean=[ 0.3 -0.4] d=2

Mean, covariance, and density#

The marginal layer reports the moments of \(X\) (which fold in the variance-mean

coupling through \(\gamma\)) and evaluates log_prob / pdf on single

observations. Skewness and excess kurtosis are closed form from the

subordinator raw moments (see The Generalized Hyperbolic Distribution):

nig = models["NormalInverseGaussian"]

print("mean:\n", np.asarray(nig.mean()))

print("cov:\n", np.asarray(nig.cov()))

print("skewness:", np.asarray(nig.skewness()))

print("excess kurtosis:", np.asarray(nig.kurtosis()))

print("log_prob at origin:", float(nig.log_prob(jnp.zeros(2))))

mean:

[ 0.3 -0.4]

cov:

[[1.06 0.22 ]

[0.22 1.1067]]

skewness: [ 0.5828 -0.7605]

excess kurtosis: [2.4528 2.7711]

log_prob at origin: -1.382585051529043

Marginal vs joint layers#

The .joint attribute exposes the \((X, Y)\) structure. The joint sampler returns

both; the marginal sampler returns only \(X\) (the same draws, with \(Y\) dropped):

X, Y = nig.joint.rvs(20_000, seed=0)

print("X:", X.shape, " Y (subordinator):", Y.shape)

print("E[Y] =", float(Y.mean()))

sub = nig.joint.subordinator() # the latent InverseGaussian

print("subordinator:", type(sub).__name__, " mean:", float(sub.mean()))

X: (20000, 2) Y (subordinator): (20000,)

E[Y] = 1.0036306784108049

subordinator: InverseGaussian mean: 1.0

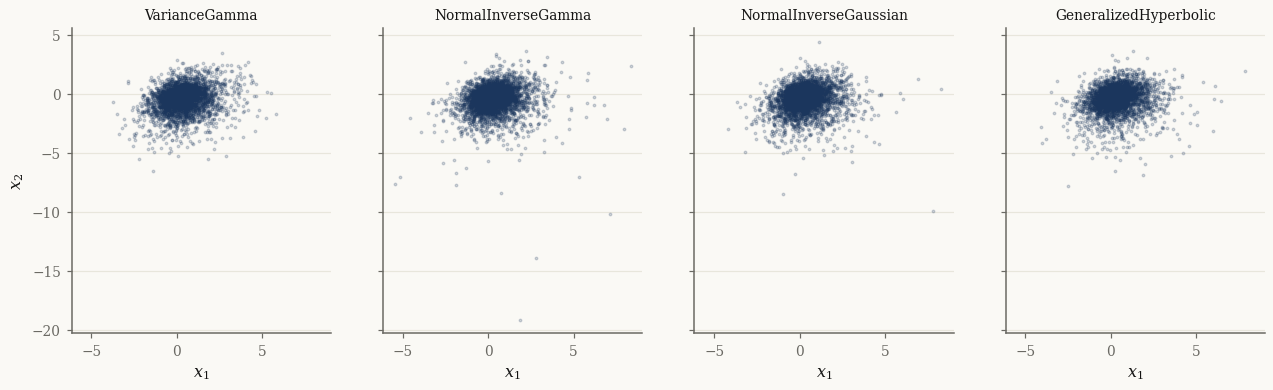

import matplotlib.pyplot as plt

fig, axes = plt.subplots(1, len(models), figsize=(14, 3.6), sharex=True, sharey=True)

for ax, (name, m) in zip(axes, models.items()):

Xs = m.rvs(4000, seed=1)

ax.scatter(np.asarray(Xs[:, 0]), np.asarray(Xs[:, 1]), s=3, alpha=0.2)

ax.set_title(name, fontsize=9); ax.set_xlabel("$x_1$")

axes[0].set_ylabel("$x_2$")

plt.show()

The univariate face: CDF and quantiles#

In one dimension the mixtures gain a scipy-style scalar API with cdf and

ppf, useful for VaR-style tail calculations. Each marginal has a matching

Univariate* class:

from normix import UnivariateNormalInverseGaussian

u = UnivariateNormalInverseGaussian.from_classical(

mu=0.0, gamma=-0.5, sigma=1.0, mu_ig=1.0, lam=1.0)

print("mean / std :", float(u.mean()), float(u.std()))

print("5% quantile:", float(u.ppf(jnp.array(0.05))))

print("cdf(ppf):", float(u.cdf(u.ppf(jnp.array(0.05)))))

mean / std : -0.5 1.118033988749895

5% quantile: -2.4957660689683925

cdf(ppf): 0.05

Fitting by EM#

fit runs the EM algorithm and returns an EMResult. Here we generate data

from the NIG model and recover it:

X_train = nig.rvs(4000, seed=42)

init = NormalInverseGaussian.default_init(X_train)

result = init.fit(X_train, max_iter=100, tol=1e-3, verbose=0)

print("converged :", result.converged)

print("iterations:", result.n_iter)

print("elapsed : %.2fs" % result.elapsed_time)

print("fitted γ :", np.asarray(result.model.gamma))

print("true γ :", np.asarray(gamma))

converged : True

iterations: 22

elapsed : 10.67s

fitted γ : [ 0.3745 -0.3682]

true γ : [ 0.3 -0.4]

The returned EMResult.model is the fitted distribution; the EM machinery

itself is covered in depth in the Batch EM in practice tutorial.

Takeaways#

The four marginals share

from_classical(mu, gamma, sigma, <subordinator params>),mean/cov,pdf/log_prob, andrvs..jointexposes the latent \((X, Y)\) pair and.joint.subordinator()the mixing distribution;joint.rvsreturns both.Univariate*variants addcdf/ppffor \(d = 1\).fitperforms EM and returns anEMResultwhose.modelis the fit.

Next: Factor mixtures for high dimensions scales these mixtures to high dimensions with a low-rank factor covariance.