Univariate positive distributions#

Gamma, InverseGamma, and InverseGaussian are the building blocks of the GH

family — they are the subordinators that drive the mixtures. They are also the

distributions with the cleanest exponential-family structure: their moments and

maximum-likelihood estimates are available in closed form, so the

log-partition triad uses analytical gradients (digamma / trigamma) rather

than autodiff.

import jax

jax.config.update("jax_enable_x64", True)

import jax.numpy as jnp

import numpy as np

from normix import Gamma, InverseGamma, InverseGaussian

from normix.utils.plotting import set_theme

set_theme()

np.set_printoptions(precision=5, suppress=True)

Construction and moments#

Each distribution is built directly from its classical parameters and reports its first two moments:

dists = {

"Gamma(α=2.5, β=1.5)": Gamma(alpha=jnp.array(2.5), beta=jnp.array(1.5)),

"InverseGamma(α=3, β=2)": InverseGamma(alpha=jnp.array(3.0), beta=jnp.array(2.0)),

"InverseGaussian(μ=1, λ=3)": InverseGaussian(mu=jnp.array(1.0), lam=jnp.array(3.0)),

}

print(f"{'distribution':28s} {'mean':>8s} {'var':>8s} {'std':>8s}")

for name, d in dists.items():

print(f"{name:28s} {float(d.mean()):8.4f} {float(d.var()):8.4f} {float(d.std()):8.4f}")

distribution mean var std

Gamma(α=2.5, β=1.5) 1.6667 1.1111 1.0541

InverseGamma(α=3, β=2) 1.0000 1.0000 1.0000

InverseGaussian(μ=1, λ=3) 1.0000 0.3333 0.5774

Density, CDF, and quantiles#

All three provide pdf, cdf, and the quantile function ppf. cdf and ppf

are mutual inverses:

d = dists["Gamma(α=2.5, β=1.5)"]

q = jnp.array([0.1, 0.5, 0.9])

x_q = jax.vmap(d.ppf)(q)

back = jax.vmap(d.cdf)(x_q)

print("quantiles x_q :", np.asarray(x_q))

print("cdf(ppf(q)) :", np.asarray(back))

quantiles x_q : [0.53677 1.45049 3.07879]

cdf(ppf(q)) : [0.1 0.5 0.9]

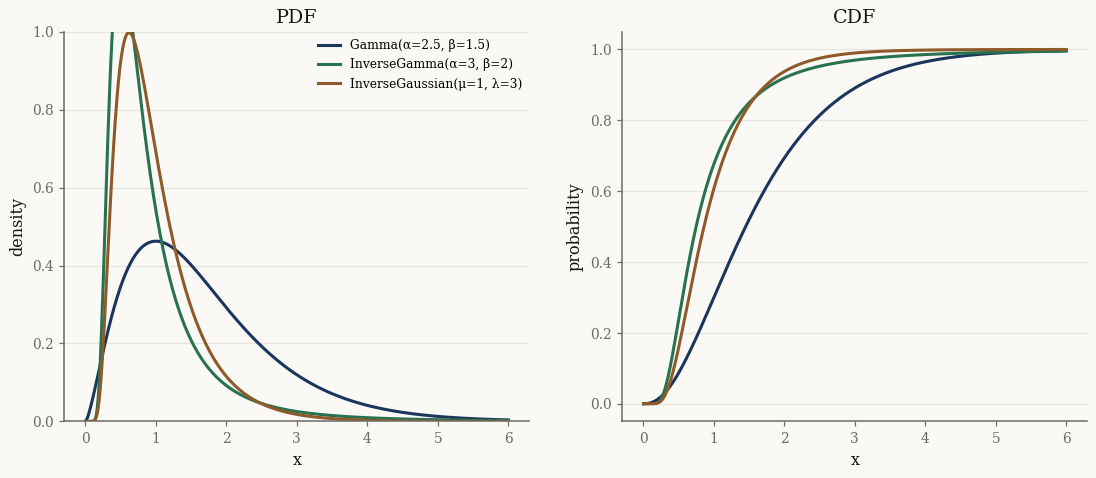

import matplotlib.pyplot as plt

x = jnp.linspace(1e-3, 6.0, 400)

fig, (axp, axc) = plt.subplots(1, 2, figsize=(12, 4.6))

for name, d in dists.items():

axp.plot(np.asarray(x), np.asarray(jax.vmap(d.pdf)(x)), label=name)

axc.plot(np.asarray(x), np.asarray(jax.vmap(d.cdf)(x)), label=name)

axp.set_title("PDF"); axp.set_xlabel("x"); axp.set_ylabel("density")

axc.set_title("CDF"); axc.set_xlabel("x"); axc.set_ylabel("probability")

axp.set_ylim(0, 1.0); axp.legend(fontsize=8)

plt.show()

Three parametrizations#

As exponential families they expose natural (\(\theta\)) and expectation

(\(\eta\)) parameters. For Gamma, \(\eta = (\mathbb{E}[\log X],\, \mathbb{E}[X])\),

and the round-trip back to classical parameters is exact:

g = dists["Gamma(α=2.5, β=1.5)"]

theta = g.natural_params()

eta = g.expectation_params()

print("theta =", np.asarray(theta))

print("eta = (E[log X], E[X]) =", np.asarray(eta))

g_back = Gamma.from_expectation(eta)

print("recovered (alpha, beta):", float(g_back.alpha), float(g_back.beta))

theta = [ 1.5 -1.5]

eta = (E[log X], E[X]) = [0.29769 1.66667]

recovered (alpha, beta): 2.5000000000000004 1.5000000000000002

Closed-form maximum likelihood#

Because the MLE matches moments, fit_mle recovers parameters from samples in a

single call. We draw from each distribution and refit:

for name, d in dists.items():

x = d.rvs(50_000, seed=0)

if isinstance(d, Gamma):

fitted = Gamma.fit_mle(x)

true_p, fit_p = (d.alpha, d.beta), (fitted.alpha, fitted.beta)

elif isinstance(d, InverseGamma):

fitted = InverseGamma.fit_mle(x)

true_p, fit_p = (d.alpha, d.beta), (fitted.alpha, fitted.beta)

else:

fitted = InverseGaussian.fit_mle(x)

true_p, fit_p = (d.mu, d.lam), (fitted.mu, fitted.lam)

true_p = tuple(round(float(v), 3) for v in true_p)

fit_p = tuple(round(float(v), 3) for v in fit_p)

print(f"{name:28s} true={true_p} mle={fit_p}")

Gamma(α=2.5, β=1.5) true=(2.5, 1.5) mle=(2.461, 1.476)

InverseGamma(α=3, β=2) true=(3.0, 2.0) mle=(2.951, 1.968)

InverseGaussian(μ=1, λ=3) true=(1.0, 3.0) mle=(1.0, 2.98)

The analytical triad means none of this routes through a generic optimizer: the

gradient of the log-partition is digamma, its Hessian is trigamma, and

from_expectation inverts them directly.

Takeaways#

Gamma,InverseGamma,InverseGaussianprovidepdf,cdf,ppf,mean/var/std, andrvs.They carry analytical log-partition gradients, so moments and

fit_mleare closed-form and fast.These three are exactly the subordinators behind VG, NInvG, and NIG.

Next: The Generalized Inverse Gaussian covers the GIG, where the log-partition involves Bessel

functions and from_expectation needs a multi-start solver.