A tour of the GH family#

The Generalized Hyperbolic (GH) distribution and its relatives are all normal variance-mean mixtures: a Gaussian whose mean and covariance are scaled by a positive latent variable \(Y\),

Different choices of the subordinator \(Y\) produce the whole family. This tutorial maps that hierarchy and shows how the pieces fit together.

import jax

jax.config.update("jax_enable_x64", True)

import jax.numpy as jnp

import numpy as np

from normix import (

Gamma, InverseGamma, InverseGaussian, GIG,

UnivariateVarianceGamma, UnivariateNormalInverseGamma,

UnivariateNormalInverseGaussian, UnivariateGeneralizedHyperbolic,

)

from normix.utils.plotting import set_theme

set_theme()

np.set_printoptions(precision=5, suppress=True)

The mixing mechanism#

Sampling is hierarchical: draw \(Y\), then draw \(X\) given \(Y\). We can reproduce a

marginal sample by hand and check it matches the built-in sampler. The joint

rvs returns both \(X\) and the latent \(Y\):

gh = UnivariateGeneralizedHyperbolic.from_classical(

mu=0.0, gamma=0.4, sigma=1.0, p=-0.5, a=1.0, b=1.0)

X, Y = gh.joint.rvs(50_000, seed=0)

print("X shape:", X.shape, " Y shape:", Y.shape)

print("E[Y] =", float(Y.mean()), " Var[Y] =", float(Y.var()))

print("skew(X) =", float(((X - X.mean())**3).mean() / X.std()**3))

X shape: (50000, 1) Y shape: (50000,)

E[Y] = 1.0080074760677304 Var[Y] = 1.0118961918124396

skew(X) = 1.137510856845186

The positive skew of \(X\) comes entirely from \(\gamma\): the variance-mean coupling tilts the Gaussian by an amount proportional to \(Y\).

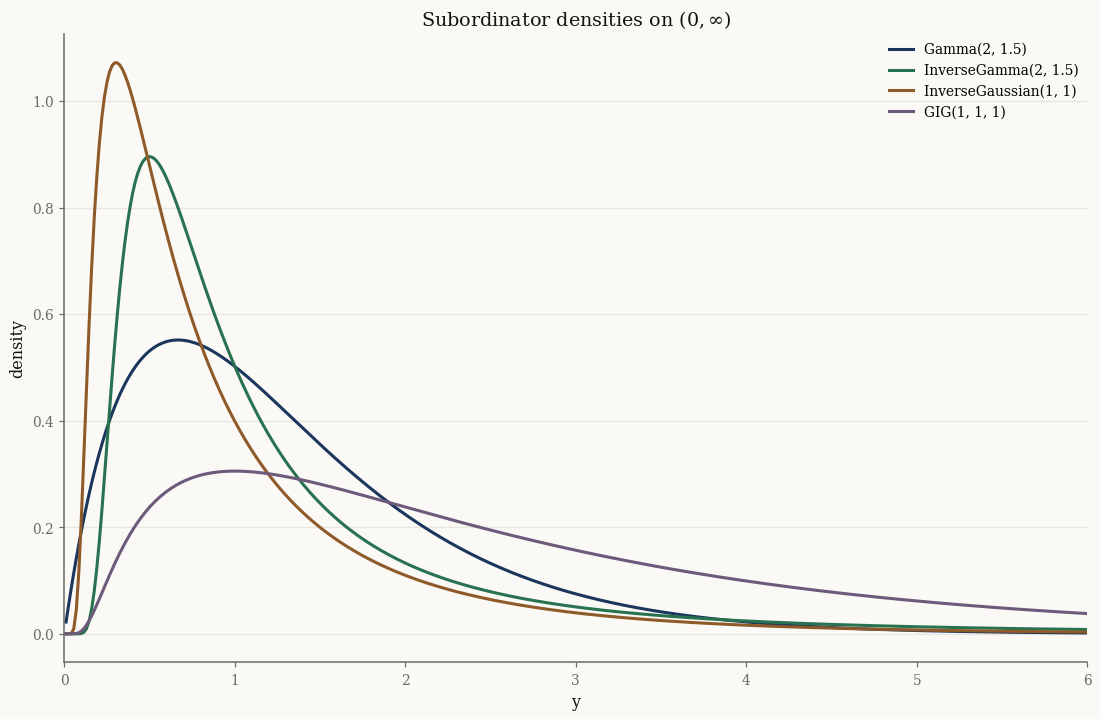

Four subordinators#

The subordinator is itself an exponential family. The four building blocks are

Gamma, InverseGamma, InverseGaussian, and the GIG (Generalized Inverse

Gaussian) that nests them all:

subs = {

"Gamma(2, 1.5)": Gamma(alpha=jnp.array(2.0), beta=jnp.array(1.5)),

"InverseGamma(2, 1.5)": InverseGamma(alpha=jnp.array(2.0), beta=jnp.array(1.5)),

"InverseGaussian(1, 1)": InverseGaussian(mu=jnp.array(1.0), lam=jnp.array(1.0)),

"GIG(1, 1, 1)": GIG(p=jnp.array(1.0), a=jnp.array(1.0), b=jnp.array(1.0)),

}

import matplotlib.pyplot as plt

y = jnp.linspace(0.01, 6.0, 400)

fig, ax = plt.subplots()

for name, s in subs.items():

ax.plot(np.asarray(y), np.asarray(jax.vmap(s.pdf)(y)), label=name)

ax.set_xlabel("y"); ax.set_ylabel("density"); ax.set_xlim(0, 6)

ax.set_title("Subordinator densities on $(0, \\infty)$")

ax.legend()

plt.show()

The GIG nests the others#

The GIG distribution with parameters \((p, a, b)\) has density on \((0,\infty)\)

proportional to \(y^{p-1}\exp\!\big(-\tfrac12(a y + b/y)\big)\). Its degenerate

limits recover the simpler subordinators exactly:

Limit |

Recovers |

|---|---|

\(b \to 0,\ p > 0\) |

\(\mathrm{Gamma}(p,\, a/2)\) |

\(a \to 0,\ p < 0\) |

\(\mathrm{InverseGamma}(-p,\, b/2)\) |

\(p = -\tfrac12\) |

\(\mathrm{InverseGaussian}\) |

x = jnp.linspace(0.05, 6.0, 300)

def max_logp_gap(d1, d2):

return float(jnp.max(jnp.abs(jax.vmap(d1.log_prob)(x) - jax.vmap(d2.log_prob)(x))))

# b -> 0, p > 0 => Gamma(p, a/2)

gap_gamma = max_logp_gap(

GIG(p=jnp.array(2.0), a=jnp.array(3.0), b=jnp.array(1e-8)),

Gamma(alpha=jnp.array(2.0), beta=jnp.array(1.5)))

# a -> 0, p < 0 => InverseGamma(-p, b/2)

gap_invgamma = max_logp_gap(

GIG(p=jnp.array(-2.0), a=jnp.array(1e-8), b=jnp.array(3.0)),

InverseGamma(alpha=jnp.array(2.0), beta=jnp.array(1.5)))

# p = -1/2 => InverseGaussian(mu, lam) with a = lam/mu^2, b = lam

mu_, lam_ = 1.5, 2.0

gap_invgauss = max_logp_gap(

GIG(p=jnp.array(-0.5), a=jnp.array(lam_ / mu_**2), b=jnp.array(lam_)),

InverseGaussian(mu=jnp.array(mu_), lam=jnp.array(lam_)))

print(f"GIG -> Gamma max|Δ log p| = {gap_gamma:.2e}")

print(f"GIG -> InverseGamma max|Δ log p| = {gap_invgamma:.2e}")

print(f"GIG -> InvGaussian max|Δ log p| = {gap_invgauss:.2e}")

GIG -> Gamma max|Δ log p| = 9.25e-08

GIG -> InverseGamma max|Δ log p| = 2.25e-08

GIG -> InvGaussian max|Δ log p| = 4.44e-15

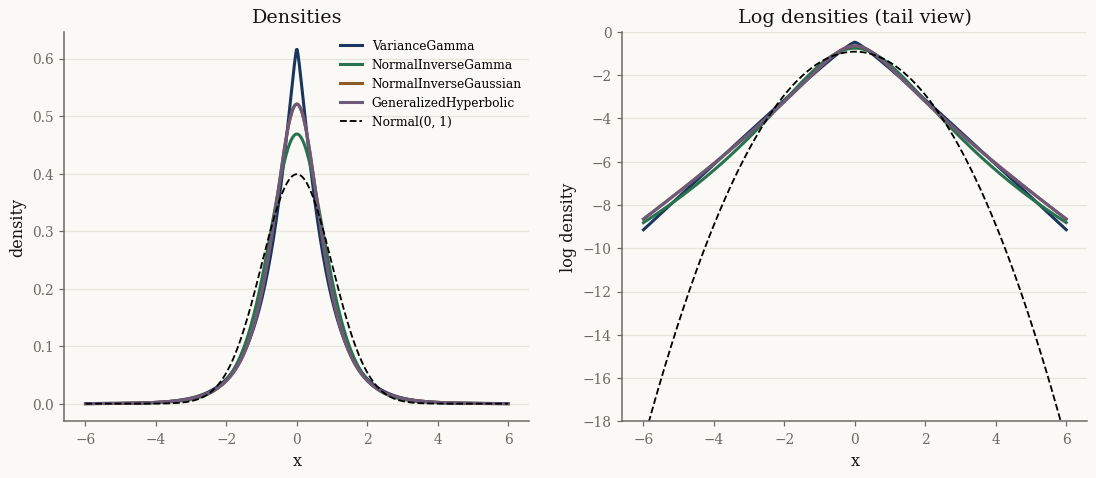

The four marginal mixtures#

Choosing each subordinator for the mixing variable yields a named marginal distribution:

Subordinator |

Marginal |

normix class |

|---|---|---|

Gamma |

Variance Gamma |

|

Inverse Gamma |

Normal-Inverse Gamma |

|

Inverse Gaussian |

Normal-Inverse Gaussian |

|

GIG |

Generalized Hyperbolic |

|

We compare them in 1-D against a standard normal, all centred and scaled to unit variance, to expose the differences in the tails:

marginals = {

"VarianceGamma": UnivariateVarianceGamma.from_classical(

mu=0.0, gamma=0.0, sigma=1.0, alpha=1.2, beta=1.2),

"NormalInverseGamma": UnivariateNormalInverseGamma.from_classical(

mu=0.0, gamma=0.0, sigma=1.0, alpha=3.0, beta=2.0),

"NormalInverseGaussian": UnivariateNormalInverseGaussian.from_classical(

mu=0.0, gamma=0.0, sigma=1.0, mu_ig=1.0, lam=1.0),

"GeneralizedHyperbolic": UnivariateGeneralizedHyperbolic.from_classical(

mu=0.0, gamma=0.0, sigma=1.0, p=-0.5, a=1.0, b=1.0),

}

for name, m in marginals.items():

print(f"{name:24s} mean={float(m.mean()):+.3f} std={float(m.std()):.3f}")

VarianceGamma mean=+0.000 std=1.000

NormalInverseGamma mean=+0.000 std=1.000

NormalInverseGaussian mean=+0.000 std=1.000

GeneralizedHyperbolic mean=+0.000 std=1.000

from jax.scipy.stats import norm

xs = jnp.linspace(-6, 6, 600)

fig, axes = plt.subplots(1, 2, figsize=(12, 4.6))

for name, m in marginals.items():

pdf = np.asarray(jax.vmap(m.pdf)(xs))

axes[0].plot(np.asarray(xs), pdf, label=name)

axes[1].plot(np.asarray(xs), np.log(pdf + 1e-300), label=name)

for ax in axes:

ax.plot(np.asarray(xs), np.asarray(norm.pdf(xs)) if ax is axes[0]

else np.asarray(norm.logpdf(xs)),

"k--", lw=1.2, label="Normal(0, 1)")

ax.set_xlabel("x")

axes[0].set_ylabel("density"); axes[0].set_title("Densities")

axes[1].set_ylabel("log density"); axes[1].set_title("Log densities (tail view)")

axes[1].set_ylim(-18, 0)

axes[0].legend(fontsize=8)

plt.show()

The log-density panel makes the point: every GH-family marginal has heavier tails than the Gaussian. Mixing over a positive \(Y\) is exactly what produces the excess kurtosis seen in financial returns and other heavy-tailed data.

Takeaways#

The GH family is the set of normal variance-mean mixtures \(X \mid Y \sim \mathcal{N}(\mu + \gamma Y, \Sigma Y)\).

The subordinator \(Y\) selects the member: Gamma → VG, Inverse Gamma → NInvG, Inverse Gaussian → NIG, GIG → GH.

The

GIGnestsGamma,InverseGamma, andInverseGaussianas limits, so GH nests all the others.Asymmetry comes from \(\gamma\); heavy tails come from the mixing.

Next: Bessel functions and log_kv digs into the Bessel function log_kv that

makes the GH densities computable, and Random sampling covers drawing

samples from every distribution.