This page was generated from a Jupyter notebook. You can view it on GitHub or download and run it locally.

Comparison of Normal Mixture Distributions

This notebook compares the normal variance-mean mixture distributions:

Distribution |

Mixing Distribution |

Tail Behavior |

|---|---|---|

Generalized Hyperbolic (GH) |

\(Y \sim \text{GIG}(p, a, b)\) |

Most general |

Variance Gamma (VG) |

\(Y \sim \text{Gamma}(\alpha, \beta)\) |

Semi-heavy |

Normal Inverse Gamma (NInvG) |

\(Y \sim \text{InvGamma}(\alpha, \beta)\) |

Heavy (Student-t like) |

Normal Inverse Gaussian (NIG) |

\(Y \sim \text{InvGauss}(\delta, \eta)\) |

Semi-heavy |

We also compare with the Normal and Student-t distributions.

Key insight: VG, NInvG, and NIG are all special cases of the Generalized Hyperbolic distribution.

[1]:

import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

from normix.distributions.mixtures import (

GeneralizedHyperbolic,

VarianceGamma,

NormalInverseGamma,

NormalInverseGaussian

)

plt.style.use('seaborn-v0_8-whitegrid')

%matplotlib inline

np.set_printoptions(precision=4, suppress=True)

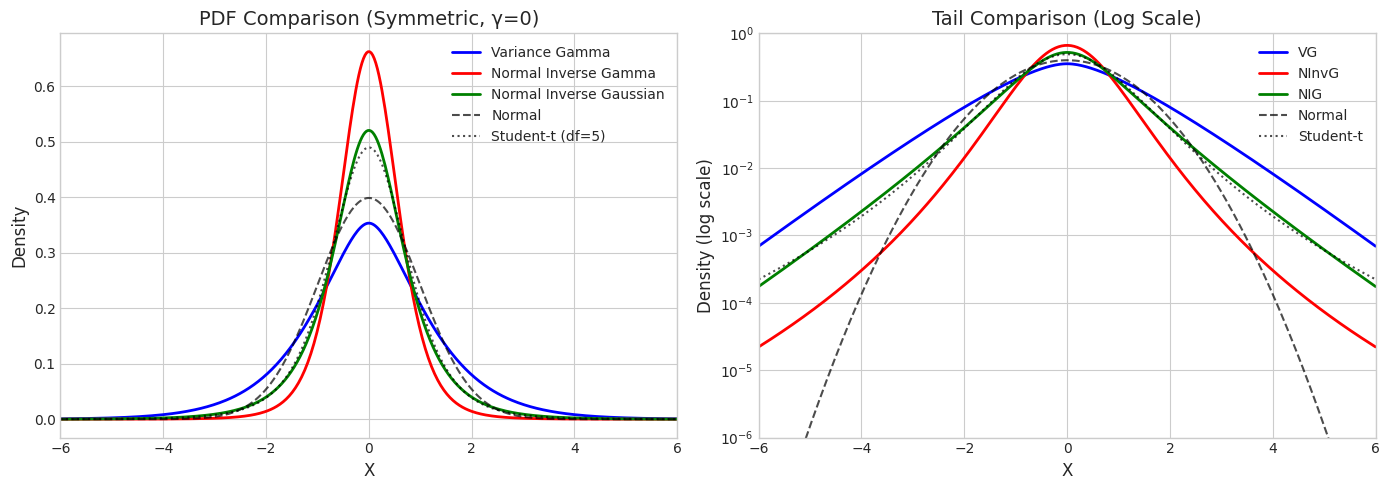

1. Symmetric Distributions (γ = 0)

When \(\gamma = 0\), all mixture distributions are symmetric. We match them to have similar variance.

[2]:

# Create symmetric distributions with similar variance

# VG: Var[X] = (α/β) σ² when γ=0, so for α=2, β=1, σ²=1, Var=2

vg_sym = VarianceGamma.from_classical_params(

mu=np.array([0.0]),

gamma=np.array([0.0]),

sigma=np.array([[1.0]]),

shape=2.0,

rate=1.0

)

# NInvG: Var[X] = (β/(α-1)) σ² when γ=0 and α>2

# For α=3, β=2, σ²=1, Var = (2/2)*1 = 1, but let's match VG variance

ninvg_sym = NormalInverseGamma.from_classical_params(

mu=np.array([0.0]),

gamma=np.array([0.0]),

sigma=np.array([[1.0]]),

shape=3.0,

rate=1.0

)

# NIG: Var[X] = δ σ² when γ=0

nig_sym = NormalInverseGaussian.from_classical_params(

mu=np.array([0.0]),

gamma=np.array([0.0]),

sigma=np.array([[1.0]]),

delta=1.0,

eta=1.0

)

print("Symmetric Distributions")

print("="*50)

print(f"VG: mean = {vg_sym.mean()[0]:.4f}, var = {vg_sym.var()[0]:.4f}")

print(f"NInvG: mean = {ninvg_sym.mean()[0]:.4f}, var = {ninvg_sym.var()[0]:.4f}")

print(f"NIG: mean = {nig_sym.mean()[0]:.4f}, var = {nig_sym.var()[0]:.4f}")

Symmetric Distributions

==================================================

VG: mean = 0.0000, var = 2.0000

NInvG: mean = 0.0000, var = 0.5000

NIG: mean = 0.0000, var = 1.0000

[3]:

# PDF comparison

x_range = np.linspace(-6, 6, 400)

vg_pdf = vg_sym.pdf(x_range.reshape(-1, 1)).flatten()

ninvg_pdf = ninvg_sym.pdf(x_range.reshape(-1, 1)).flatten()

nig_pdf = nig_sym.pdf(x_range.reshape(-1, 1)).flatten()

# Match variance for Normal and Student-t

var_ref = 1.0 # Use unit variance for comparison

normal_pdf = stats.norm(0, np.sqrt(var_ref)).pdf(x_range)

t_pdf = stats.t(df=5, scale=np.sqrt(var_ref * 3/5)).pdf(x_range) # df=5, scaled for same variance

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Linear scale

axes[0].plot(x_range, vg_pdf, 'b-', linewidth=2, label='Variance Gamma')

axes[0].plot(x_range, ninvg_pdf, 'r-', linewidth=2, label='Normal Inverse Gamma')

axes[0].plot(x_range, nig_pdf, 'g-', linewidth=2, label='Normal Inverse Gaussian')

axes[0].plot(x_range, normal_pdf, 'k--', linewidth=1.5, alpha=0.7, label='Normal')

axes[0].plot(x_range, t_pdf, 'k:', linewidth=1.5, alpha=0.7, label='Student-t (df=5)')

axes[0].set_xlabel('X', fontsize=12)

axes[0].set_ylabel('Density', fontsize=12)

axes[0].set_title('PDF Comparison (Symmetric, γ=0)', fontsize=14)

axes[0].legend()

axes[0].set_xlim(-6, 6)

# Log scale for tail comparison

axes[1].semilogy(x_range, vg_pdf, 'b-', linewidth=2, label='VG')

axes[1].semilogy(x_range, ninvg_pdf, 'r-', linewidth=2, label='NInvG')

axes[1].semilogy(x_range, nig_pdf, 'g-', linewidth=2, label='NIG')

axes[1].semilogy(x_range, normal_pdf, 'k--', linewidth=1.5, alpha=0.7, label='Normal')

axes[1].semilogy(x_range, t_pdf, 'k:', linewidth=1.5, alpha=0.7, label='Student-t')

axes[1].set_xlabel('X', fontsize=12)

axes[1].set_ylabel('Density (log scale)', fontsize=12)

axes[1].set_title('Tail Comparison (Log Scale)', fontsize=14)

axes[1].legend()

axes[1].set_xlim(-6, 6)

axes[1].set_ylim(1e-6, 1)

plt.tight_layout()

plt.show()

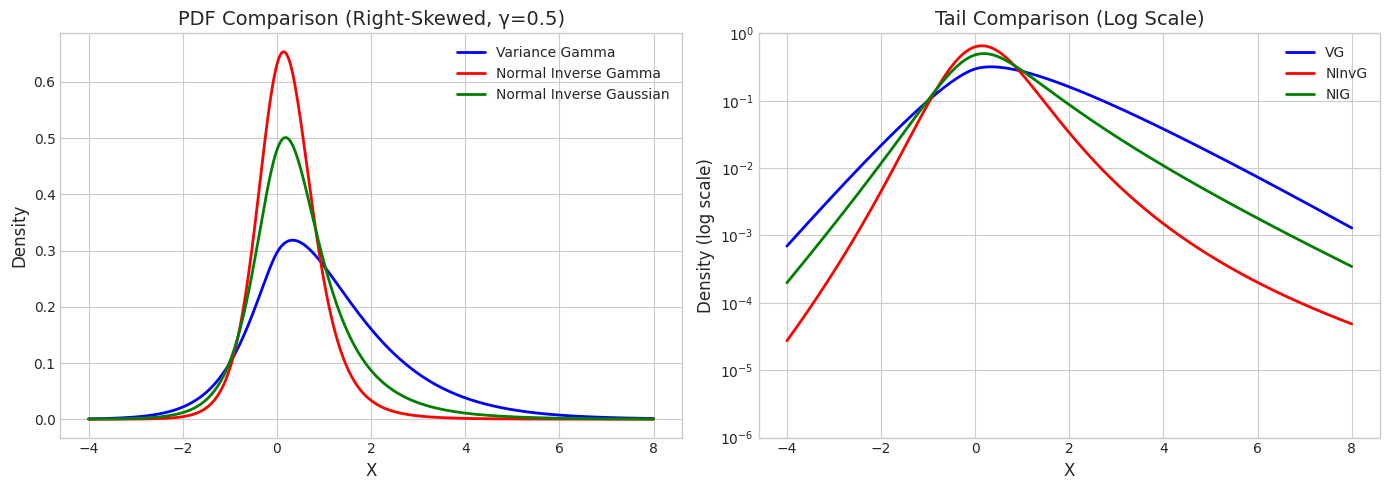

2. Skewed Distributions (γ ≠ 0)

When \(\gamma \neq 0\), the distributions become asymmetric.

[4]:

# Create right-skewed distributions

gamma_val = 0.5

vg_skew = VarianceGamma.from_classical_params(

mu=np.array([0.0]),

gamma=np.array([gamma_val]),

sigma=np.array([[1.0]]),

shape=2.0,

rate=1.0

)

ninvg_skew = NormalInverseGamma.from_classical_params(

mu=np.array([0.0]),

gamma=np.array([gamma_val]),

sigma=np.array([[1.0]]),

shape=3.0,

rate=1.0

)

nig_skew = NormalInverseGaussian.from_classical_params(

mu=np.array([0.0]),

gamma=np.array([gamma_val]),

sigma=np.array([[1.0]]),

delta=1.0,

eta=1.0

)

print(f"Right-Skewed Distributions (γ = {gamma_val})")

print("="*50)

print(f"VG: mean = {vg_skew.mean()[0]:.4f}, var = {vg_skew.var()[0]:.4f}")

print(f"NInvG: mean = {ninvg_skew.mean()[0]:.4f}, var = {ninvg_skew.var()[0]:.4f}")

print(f"NIG: mean = {nig_skew.mean()[0]:.4f}, var = {nig_skew.var()[0]:.4f}")

Right-Skewed Distributions (γ = 0.5)

==================================================

VG: mean = 1.0000, var = 2.5000

NInvG: mean = 0.2500, var = 0.5625

NIG: mean = 0.5000, var = 1.2500

[5]:

# PDF comparison - skewed

x_range = np.linspace(-4, 8, 400)

vg_pdf = vg_skew.pdf(x_range.reshape(-1, 1)).flatten()

ninvg_pdf = ninvg_skew.pdf(x_range.reshape(-1, 1)).flatten()

nig_pdf = nig_skew.pdf(x_range.reshape(-1, 1)).flatten()

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Linear scale

axes[0].plot(x_range, vg_pdf, 'b-', linewidth=2, label='Variance Gamma')

axes[0].plot(x_range, ninvg_pdf, 'r-', linewidth=2, label='Normal Inverse Gamma')

axes[0].plot(x_range, nig_pdf, 'g-', linewidth=2, label='Normal Inverse Gaussian')

axes[0].set_xlabel('X', fontsize=12)

axes[0].set_ylabel('Density', fontsize=12)

axes[0].set_title(f'PDF Comparison (Right-Skewed, γ={gamma_val})', fontsize=14)

axes[0].legend()

# Log scale for tail comparison

axes[1].semilogy(x_range, vg_pdf, 'b-', linewidth=2, label='VG')

axes[1].semilogy(x_range, ninvg_pdf, 'r-', linewidth=2, label='NInvG')

axes[1].semilogy(x_range, nig_pdf, 'g-', linewidth=2, label='NIG')

axes[1].set_xlabel('X', fontsize=12)

axes[1].set_ylabel('Density (log scale)', fontsize=12)

axes[1].set_title('Tail Comparison (Log Scale)', fontsize=14)

axes[1].legend()

axes[1].set_ylim(1e-6, 1)

plt.tight_layout()

plt.show()

3. Sample Statistics Comparison

[6]:

# Generate samples and compute statistics

n_samples = 100000

vg_samples = vg_sym.rvs(size=n_samples, random_state=42).flatten()

ninvg_samples = ninvg_sym.rvs(size=n_samples, random_state=42).flatten()

nig_samples = nig_sym.rvs(size=n_samples, random_state=42).flatten()

normal_samples = stats.norm(0, 1).rvs(size=n_samples, random_state=42)

print("Sample Statistics (Symmetric Distributions)")

print("="*70)

print(f"{'Distribution':<15} {'Mean':>10} {'Std':>10} {'Skewness':>12} {'Kurtosis':>12}")

print("-"*70)

for name, samples in [('VG', vg_samples), ('NInvG', ninvg_samples),

('NIG', nig_samples), ('Normal', normal_samples)]:

print(f"{name:<15} {np.mean(samples):>10.4f} {np.std(samples):>10.4f} "

f"{stats.skew(samples):>12.4f} {stats.kurtosis(samples):>12.4f}")

Sample Statistics (Symmetric Distributions)

======================================================================

Distribution Mean Std Skewness Kurtosis

----------------------------------------------------------------------

VG 0.0036 1.4115 -0.0003 1.5262

NInvG 0.0011 0.7070 -0.0416 2.5453

NIG 0.0023 0.9982 0.0319 2.9578

Normal 0.0010 1.0009 -0.0018 -0.0080

[7]:

# Histogram comparison

fig, axes = plt.subplots(2, 2, figsize=(12, 10))

bins = np.linspace(-6, 6, 80)

for ax, (name, samples, color) in zip(axes.flat,

[('Variance Gamma', vg_samples, 'blue'),

('Normal Inverse Gamma', ninvg_samples, 'red'),

('Normal Inverse Gaussian', nig_samples, 'green'),

('Normal', normal_samples, 'gray')]):

ax.hist(samples, bins=bins, density=True, alpha=0.7, color=color, label='Samples')

ax.set_title(name, fontsize=12)

ax.set_xlabel('X')

ax.set_ylabel('Density')

ax.set_xlim(-6, 6)

# Add kurtosis annotation

kurt = stats.kurtosis(samples)

ax.annotate(f'Kurtosis: {kurt:.2f}', xy=(0.95, 0.95), xycoords='axes fraction',

ha='right', va='top', fontsize=10,

bbox=dict(boxstyle='round', facecolor='white', alpha=0.8))

plt.suptitle('Sample Distributions Comparison', fontsize=14)

plt.tight_layout()

plt.show()

4. Tail Behavior Analysis

Analyzing the probability of extreme events (tail probabilities).

[8]:

# Compute tail probabilities P(|X| > t) for various thresholds

thresholds = [2, 3, 4, 5]

print("Tail Probabilities P(|X| > t)")

print("="*70)

print(f"{'t':>6} {'VG':>12} {'NInvG':>12} {'NIG':>12} {'Normal':>12} {'Student-t':>12}")

print("-"*70)

normal_dist = stats.norm(0, 1)

t_dist = stats.t(df=5, scale=np.sqrt(3/5)) # Scaled to have similar variance

for t in thresholds:

vg_tail = np.mean(np.abs(vg_samples) > t)

ninvg_tail = np.mean(np.abs(ninvg_samples) > t)

nig_tail = np.mean(np.abs(nig_samples) > t)

normal_tail = 2 * normal_dist.sf(t)

t_tail = 2 * t_dist.sf(t)

print(f"{t:>6} {vg_tail:>12.6f} {ninvg_tail:>12.6f} {nig_tail:>12.6f} "

f"{normal_tail:>12.6f} {t_tail:>12.6f}")

Tail Probabilities P(|X| > t)

======================================================================

t VG NInvG NIG Normal Student-t

----------------------------------------------------------------------

2 0.141580 0.013090 0.054240 0.045500 0.049313

3 0.044780 0.002020 0.013660 0.002700 0.011725

4 0.013710 0.000390 0.003590 0.000063 0.003573

5 0.003900 0.000080 0.000800 0.000001 0.001328

[9]:

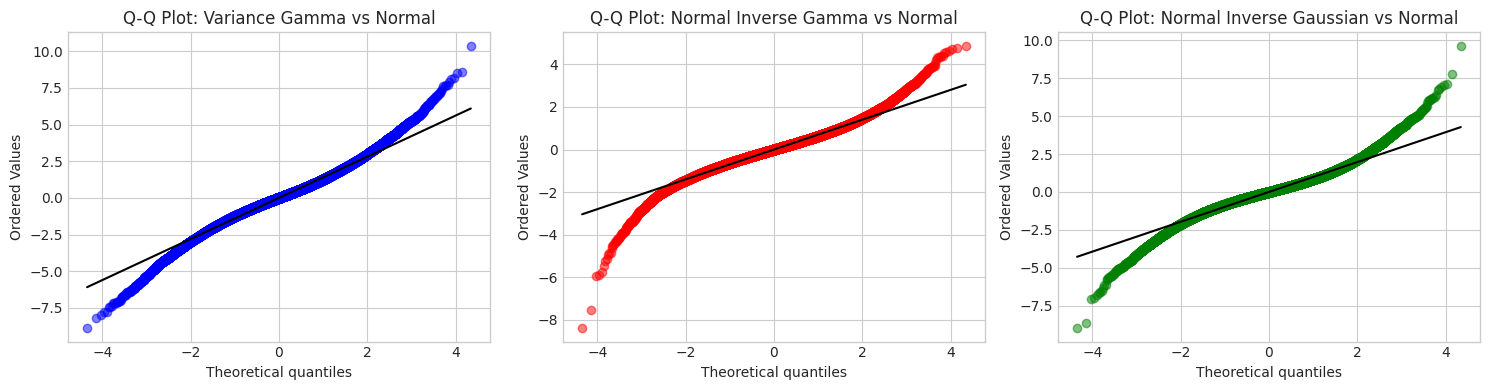

# Q-Q plots against Normal

fig, axes = plt.subplots(1, 3, figsize=(15, 4))

for ax, (name, samples, color) in zip(axes,

[('Variance Gamma', vg_samples, 'blue'),

('Normal Inverse Gamma', ninvg_samples, 'red'),

('Normal Inverse Gaussian', nig_samples, 'green')]):

stats.probplot(samples, dist='norm', plot=ax)

ax.set_title(f'Q-Q Plot: {name} vs Normal', fontsize=12)

ax.get_lines()[0].set_color(color)

ax.get_lines()[0].set_alpha(0.5)

ax.get_lines()[1].set_color('black')

plt.tight_layout()

plt.show()

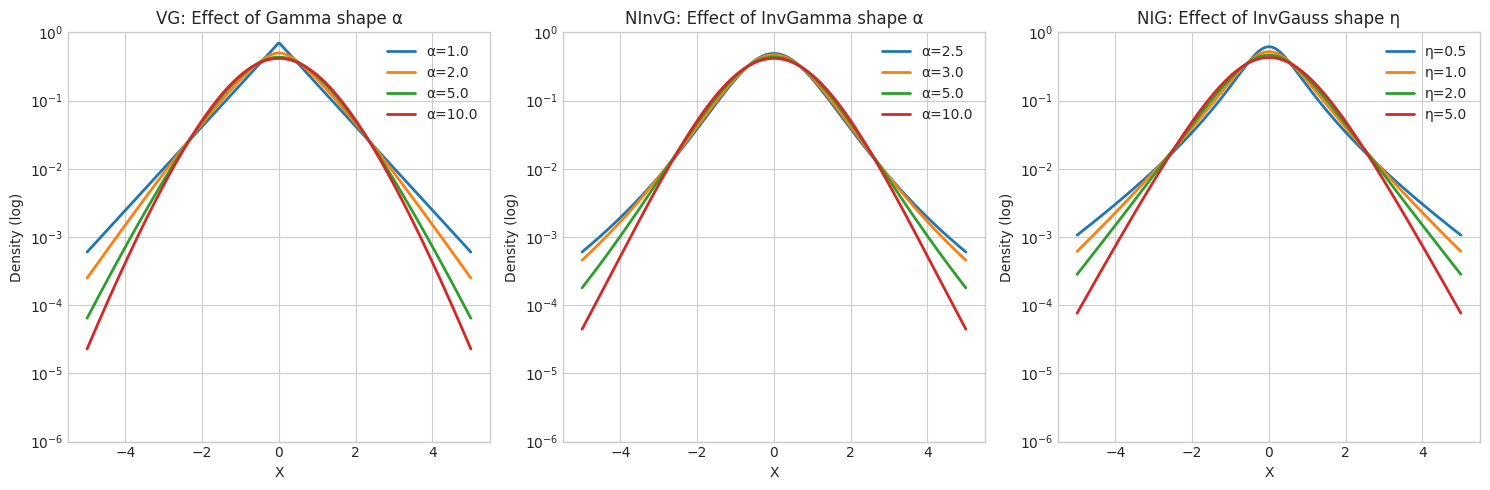

5. Effect of Mixing Distribution Parameters

[10]:

# Show how mixing distribution shape affects tails

fig, axes = plt.subplots(1, 3, figsize=(15, 5))

x_range = np.linspace(-5, 5, 300)

# VG: vary α (shape of Gamma mixing)

ax = axes[0]

for alpha in [1.0, 2.0, 5.0, 10.0]:

vg = VarianceGamma.from_classical_params(

mu=np.array([0.0]), gamma=np.array([0.0]), sigma=np.array([[1.0]]),

shape=alpha, rate=alpha # Keep E[Y]=1 constant

)

pdf = vg.pdf(x_range.reshape(-1, 1)).flatten()

ax.semilogy(x_range, pdf, linewidth=2, label=f'α={alpha}')

ax.set_xlabel('X')

ax.set_ylabel('Density (log)')

ax.set_title('VG: Effect of Gamma shape α')

ax.legend()

ax.set_ylim(1e-6, 1)

# NInvG: vary α (shape of InvGamma mixing)

ax = axes[1]

for alpha in [2.5, 3.0, 5.0, 10.0]:

ninvg = NormalInverseGamma.from_classical_params(

mu=np.array([0.0]), gamma=np.array([0.0]), sigma=np.array([[1.0]]),

shape=alpha, rate=alpha-1 # Keep E[Y]=1 constant (for α>1)

)

pdf = ninvg.pdf(x_range.reshape(-1, 1)).flatten()

ax.semilogy(x_range, pdf, linewidth=2, label=f'α={alpha}')

ax.set_xlabel('X')

ax.set_ylabel('Density (log)')

ax.set_title('NInvG: Effect of InvGamma shape α')

ax.legend()

ax.set_ylim(1e-6, 1)

# NIG: vary η (shape of InvGaussian mixing)

ax = axes[2]

for eta in [0.5, 1.0, 2.0, 5.0]:

nig = NormalInverseGaussian.from_classical_params(

mu=np.array([0.0]), gamma=np.array([0.0]), sigma=np.array([[1.0]]),

delta=1.0, eta=eta

)

pdf = nig.pdf(x_range.reshape(-1, 1)).flatten()

ax.semilogy(x_range, pdf, linewidth=2, label=f'η={eta}')

ax.set_xlabel('X')

ax.set_ylabel('Density (log)')

ax.set_title('NIG: Effect of InvGauss shape η')

ax.legend()

ax.set_ylim(1e-6, 1)

plt.tight_layout()

plt.show()

6. Summary Table

[11]:

print("\n" + "="*80)

print("SUMMARY: Normal Variance-Mean Mixture Distributions")

print("="*80)

summary = """

╔══════════════════════╦══════════════════════╦══════════════════════════════╗

║ Distribution ║ Mixing Y ║ Key Characteristics ║

╠══════════════════════╬══════════════════════╬══════════════════════════════╣

║ Variance Gamma ║ Gamma(α, β) ║ • Semi-heavy tails ║

║ ║ ║ • Flexible kurtosis ║

║ ║ ║ • Popular in finance ║

╠══════════════════════╬══════════════════════╬══════════════════════════════╣

║ Normal Inverse Gamma ║ InvGamma(α, β) ║ • Heavy tails (Student-t) ║

║ ║ ║ • Requires α > 2 for var ║

║ ║ ║ • Good for outlier-prone ║

╠══════════════════════╬══════════════════════╬══════════════════════════════╣

║ Normal Inverse ║ InvGauss(δ, η) ║ • Semi-heavy tails ║

║ Gaussian ║ ║ • Special case of GH (p=-½) ║

║ ║ ║ • Good fit for asset returns ║

╚══════════════════════╩══════════════════════╩══════════════════════════════╝

Common Properties:

• All are normal variance-mean mixtures: X|Y ~ N(μ + γY, ΣY)

• Joint distribution (X,Y) is exponential family → closed-form MLE

• Marginal distribution f(x) is NOT exponential family → requires EM

• Skewness controlled by γ (γ=0 → symmetric)

• All have heavier tails than Normal distribution

"""

print(summary)

================================================================================

SUMMARY: Normal Variance-Mean Mixture Distributions

================================================================================

╔══════════════════════╦══════════════════════╦══════════════════════════════╗

║ Distribution ║ Mixing Y ║ Key Characteristics ║

╠══════════════════════╬══════════════════════╬══════════════════════════════╣

║ Variance Gamma ║ Gamma(α, β) ║ • Semi-heavy tails ║

║ ║ ║ • Flexible kurtosis ║

║ ║ ║ • Popular in finance ║

╠══════════════════════╬══════════════════════╬══════════════════════════════╣

║ Normal Inverse Gamma ║ InvGamma(α, β) ║ • Heavy tails (Student-t) ║

║ ║ ║ • Requires α > 2 for var ║

║ ║ ║ • Good for outlier-prone ║

╠══════════════════════╬══════════════════════╬══════════════════════════════╣

║ Normal Inverse ║ InvGauss(δ, η) ║ • Semi-heavy tails ║

║ Gaussian ║ ║ • Special case of GH (p=-½) ║

║ ║ ║ • Good fit for asset returns ║

╚══════════════════════╩══════════════════════╩══════════════════════════════╝

Common Properties:

• All are normal variance-mean mixtures: X|Y ~ N(μ + γY, ΣY)

• Joint distribution (X,Y) is exponential family → closed-form MLE

• Marginal distribution f(x) is NOT exponential family → requires EM

• Skewness controlled by γ (γ=0 → symmetric)

• All have heavier tails than Normal distribution

6. Generalized Hyperbolic: The Unifying Distribution

The Generalized Hyperbolic (GH) distribution is the most general normal variance-mean mixture. All other distributions are special cases:

Special Case |

GIG Parameters |

Condition |

|---|---|---|

Variance Gamma |

\(b \to 0\), \(p > 0\) |

Gamma mixing |

Normal-Inverse Gaussian |

\(p = -1/2\) |

IG mixing |

Normal-Inverse Gamma |

\(a \to 0\), \(p < 0\) |

InvGamma mixing |

[12]:

# Create a general GH distribution

gh = GeneralizedHyperbolic.from_classical_params(

mu=np.array([0.0]),

gamma=np.array([0.5]),

sigma=np.array([[1.0]]),

p=1.0,

a=1.0,

b=1.0

)

print("Generalized Hyperbolic distribution created.")

print(f"Mean: {gh.mean()[0]:.4f}")

print(f"Variance: {gh.var()[0]:.4f}")

Generalized Hyperbolic distribution created.

Mean: 1.3497

Variance: 3.8272

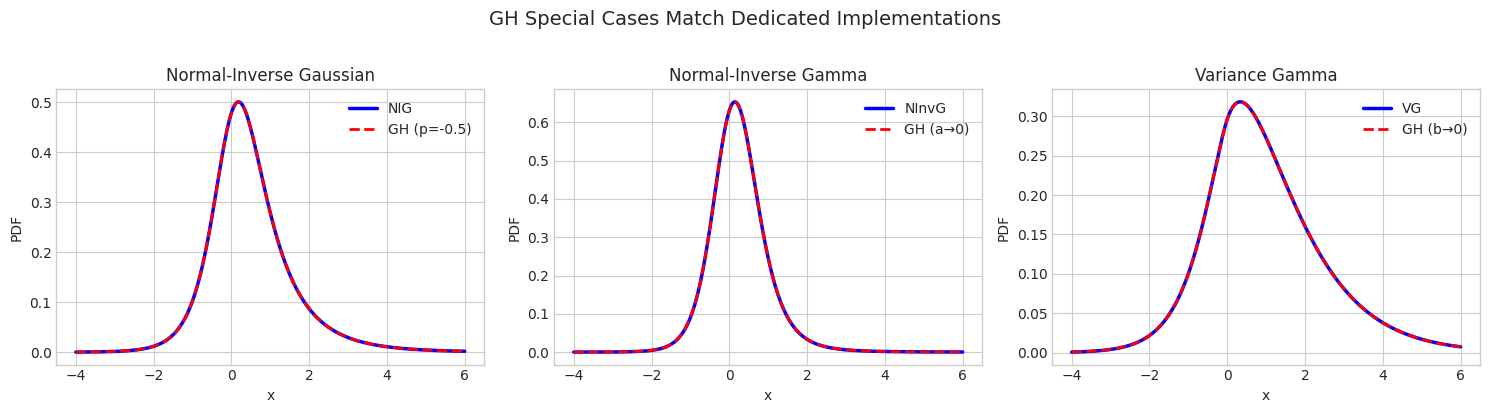

6.1 Verifying Special Cases

[13]:

# Test parameters

mu = np.array([0.0])

gamma = np.array([0.5])

sigma = np.array([[1.0]])

x = np.linspace(-4, 6, 300)

fig, axes = plt.subplots(1, 3, figsize=(15, 4))

# NIG comparison

ax = axes[0]

nig_params = {'delta': 1.0, 'eta': 1.0}

nig = NormalInverseGaussian.from_classical_params(mu=mu, gamma=gamma, sigma=sigma, **nig_params)

gh_nig = GeneralizedHyperbolic.as_normal_inverse_gaussian(mu=mu, gamma=gamma, sigma=sigma, **nig_params)

nig_pdf = nig.pdf(x.reshape(-1, 1)).flatten()

gh_nig_pdf = np.array([gh_nig.pdf(np.array([xi])) for xi in x])

ax.plot(x, nig_pdf, 'b-', linewidth=2.5, label='NIG')

ax.plot(x, gh_nig_pdf, 'r--', linewidth=2, label='GH (p=-0.5)')

ax.set_title('Normal-Inverse Gaussian', fontsize=12)

ax.set_xlabel('x')

ax.set_ylabel('PDF')

ax.legend()

# NInvG comparison

ax = axes[1]

ninvg_params = {'shape': 3.0, 'rate': 1.0}

ninvg = NormalInverseGamma.from_classical_params(mu=mu, gamma=gamma, sigma=sigma, **ninvg_params)

gh_ninvg = GeneralizedHyperbolic.as_normal_inverse_gamma(mu=mu, gamma=gamma, sigma=sigma, **ninvg_params)

ninvg_pdf = ninvg.pdf(x.reshape(-1, 1)).flatten()

gh_ninvg_pdf = np.array([gh_ninvg.pdf(np.array([xi])) for xi in x])

ax.plot(x, ninvg_pdf, 'b-', linewidth=2.5, label='NInvG')

ax.plot(x, gh_ninvg_pdf, 'r--', linewidth=2, label='GH (a→0)')

ax.set_title('Normal-Inverse Gamma', fontsize=12)

ax.set_xlabel('x')

ax.set_ylabel('PDF')

ax.legend()

# VG comparison

ax = axes[2]

vg_params = {'shape': 2.0, 'rate': 1.0}

vg = VarianceGamma.from_classical_params(mu=mu, gamma=gamma, sigma=sigma, **vg_params)

gh_vg = GeneralizedHyperbolic.as_variance_gamma(mu=mu, gamma=gamma, sigma=sigma, **vg_params)

vg_pdf = vg.pdf(x.reshape(-1, 1)).flatten()

gh_vg_pdf = np.array([gh_vg.pdf(np.array([xi])) for xi in x])

ax.plot(x, vg_pdf, 'b-', linewidth=2.5, label='VG')

ax.plot(x, gh_vg_pdf, 'r--', linewidth=2, label='GH (b→0)')

ax.set_title('Variance Gamma', fontsize=12)

ax.set_xlabel('x')

ax.set_ylabel('PDF')

ax.legend()

plt.suptitle('GH Special Cases Match Dedicated Implementations', fontsize=14, y=1.02)

plt.tight_layout()

plt.show()

[14]:

# Quantitative comparison of means

print("=" * 60)

print("Mean Comparison: GH Special Cases vs Dedicated Implementations")

print("=" * 60)

print(f"\nNIG: NIG mean = {nig.mean()[0]:.6f}, GH(p=-0.5) mean = {gh_nig.mean()[0]:.6f}")

print(f"NInvG: NInvG mean = {ninvg.mean()[0]:.6f}, GH(a→0) mean = {gh_ninvg.mean()[0]:.6f}")

print(f"VG: VG mean = {vg.mean()[0]:.6f}, GH(b→0) mean = {gh_vg.mean()[0]:.6f}")

============================================================

Mean Comparison: GH Special Cases vs Dedicated Implementations

============================================================

NIG: NIG mean = 0.500000, GH(p=-0.5) mean = 0.500000

NInvG: NInvG mean = 0.250000, GH(a→0) mean = 0.250000

VG: VG mean = 1.000000, GH(b→0) mean = 1.000000

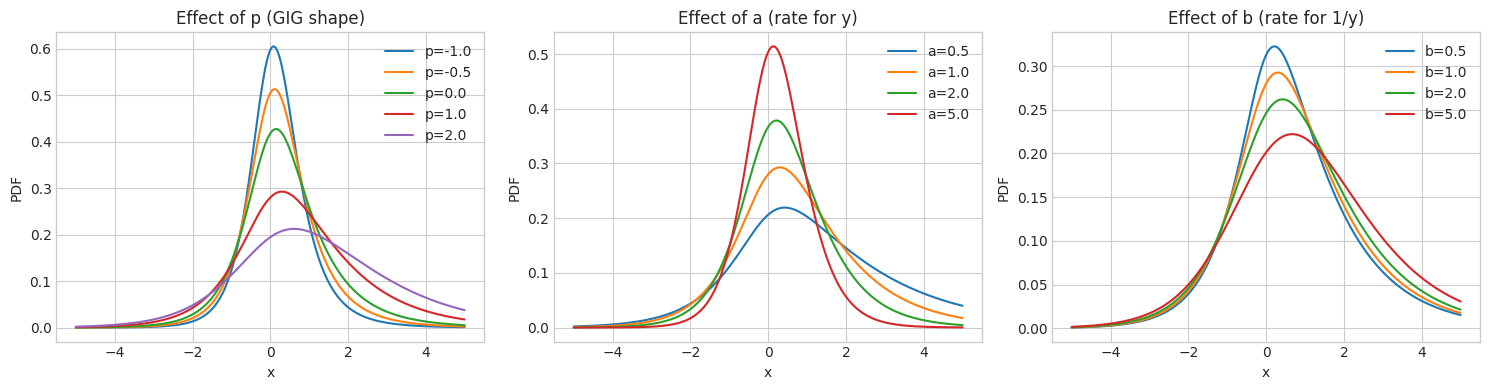

6.2 Effect of GIG Parameters

[15]:

# Effect of GIG parameters on GH distribution

fig, axes = plt.subplots(1, 3, figsize=(15, 4))

x = np.linspace(-5, 5, 300)

base_mu = np.array([0.0])

base_gamma = np.array([0.3])

base_sigma = np.array([[1.0]])

# Effect of p

ax = axes[0]

for p in [-1.0, -0.5, 0.0, 1.0, 2.0]:

try:

gh = GeneralizedHyperbolic.from_classical_params(

mu=base_mu, gamma=base_gamma, sigma=base_sigma, p=p, a=1.0, b=1.0

)

pdf = np.array([gh.pdf(np.array([xi])) for xi in x])

ax.plot(x, pdf, label=f'p={p}')

except:

pass

ax.set_title('Effect of p (GIG shape)', fontsize=12)

ax.set_xlabel('x')

ax.set_ylabel('PDF')

ax.legend()

# Effect of a

ax = axes[1]

for a in [0.5, 1.0, 2.0, 5.0]:

try:

gh = GeneralizedHyperbolic.from_classical_params(

mu=base_mu, gamma=base_gamma, sigma=base_sigma, p=1.0, a=a, b=1.0

)

pdf = np.array([gh.pdf(np.array([xi])) for xi in x])

ax.plot(x, pdf, label=f'a={a}')

except:

pass

ax.set_title('Effect of a (rate for y)', fontsize=12)

ax.set_xlabel('x')

ax.set_ylabel('PDF')

ax.legend()

# Effect of b

ax = axes[2]

for b in [0.5, 1.0, 2.0, 5.0]:

try:

gh = GeneralizedHyperbolic.from_classical_params(

mu=base_mu, gamma=base_gamma, sigma=base_sigma, p=1.0, a=1.0, b=b

)

pdf = np.array([gh.pdf(np.array([xi])) for xi in x])

ax.plot(x, pdf, label=f'b={b}')

except:

pass

ax.set_title('Effect of b (rate for 1/y)', fontsize=12)

ax.set_xlabel('x')

ax.set_ylabel('PDF')

ax.legend()

plt.tight_layout()

plt.show()

Summary

All distributions in this family are normal variance-mean mixtures

NInvG has the heaviest tails (similar to Student-t)

VG and NIG have semi-heavy tails

Skewness is controlled by the \(\gamma\) parameter

GH is the most general form, unifying all special cases