This page was generated from a Jupyter notebook. You can view it on GitHub or download and run it locally.

Generalized Hyperbolic (GH) Distribution

The Generalized Hyperbolic distribution is the most general form of the normal variance-mean mixture family.

Definition

A random variable \(X\) follows a Generalized Hyperbolic distribution if it can be written as:

where:

\(Z \sim N(0, \Sigma)\) is independent of \(Y\)

\(Y \sim \text{GIG}(p, a, b)\) (Generalized Inverse Gaussian)

Special Cases

Distribution |

GIG Parameters |

Mixing Distribution |

|---|---|---|

Variance Gamma |

\(b \to 0\), \(p > 0\) |

Gamma\((p, a/2)\) |

Normal-Inverse Gaussian |

\(p = -1/2\) |

InverseGaussian\((\delta, \eta)\) |

Normal-Inverse Gamma |

\(a \to 0\), \(p < 0\) |

InverseGamma\((-p, b/2)\) |

Hyperbolic |

\(p = 1\) |

GIG\((1, a, b)\) |

Key Properties

Joint distribution \(f(x, y)\) is an exponential family

Marginal distribution \(f(x)\) is NOT an exponential family

Fitting uses the EM algorithm with parameter regularization

[1]:

import numpy as np

import matplotlib.pyplot as plt

from matplotlib.gridspec import GridSpec

from scipy import stats

from normix.distributions.mixtures import (

GeneralizedHyperbolic, JointGeneralizedHyperbolic,

VarianceGamma, NormalInverseGaussian, NormalInverseGamma

)

from normix.utils import (

plot_joint_distribution_1d, plot_marginal_distribution_2d,

validate_moments, print_moment_validation,

fit_and_track_convergence, plot_em_convergence,

test_joint_fitting, print_fitting_results

)

plt.style.use('seaborn-v0_8-whitegrid')

%matplotlib inline

print("Imports successful!")

Imports successful!

1. Joint Distribution: \(f(x, y)\) (Exponential Family)

The joint distribution is:

where:

\(X|Y \sim N(\mu + \gamma Y, \Sigma Y)\)

\(Y \sim \text{GIG}(p, a, b)\)

[2]:

# Define parameters for 1D joint distribution

params_1d = {

'mu': np.array([0.0]),

'gamma': np.array([0.5]),

'sigma': np.array([[1.0]]),

'p': 1.0,

'a': 1.0,

'b': 1.0

}

# Create joint distribution

jgh_1d = JointGeneralizedHyperbolic.from_classical_params(**params_1d)

print("Created:", jgh_1d)

print("\nClassical parameters:", jgh_1d.classical_params)

Created: JointGeneralizedHyperbolic(μ=0.000, γ=0.500, p=1.000, a=1.000, b=1.000)

Classical parameters: GHParams(mu=array([0.]), gamma=array([0.5]), sigma=array([[1.]]), p=np.float64(1.0), a=np.float64(1.0), b=np.float64(1.0))

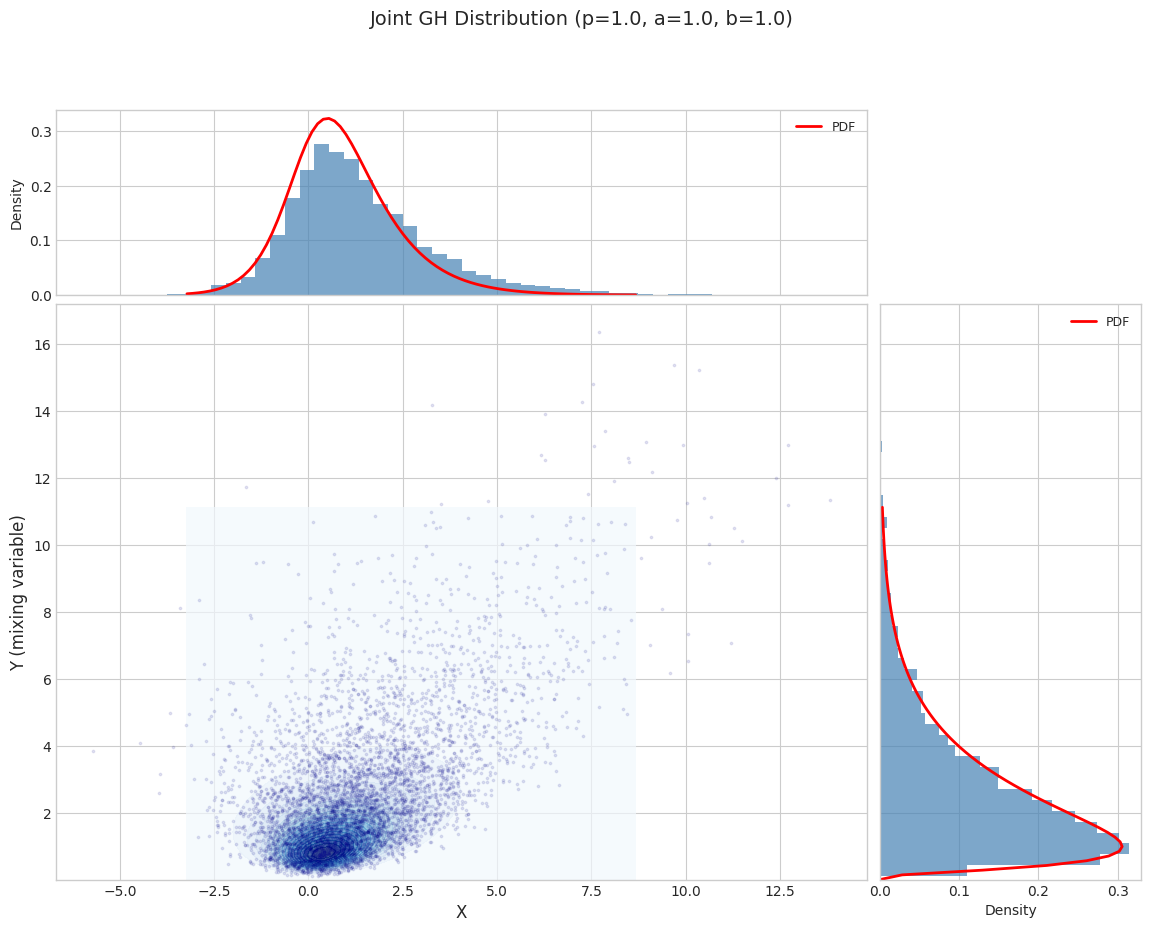

[3]:

# Visualize joint distribution

fig = plot_joint_distribution_1d(

jgh_1d, n_samples=5000, random_state=42,

title=f"Joint GH Distribution (p={params_1d['p']}, a={params_1d['a']}, b={params_1d['b']})"

)

plt.tight_layout()

plt.show()

/tmp/ipykernel_2346057/2167798511.py:6: UserWarning: This figure includes Axes that are not compatible with tight_layout, so results might be incorrect.

plt.tight_layout()

1.1 Moment Validation

[4]:

# Validate moments

moment_results = validate_moments(jgh_1d, n_samples=20000, random_state=42, is_joint=True)

print_moment_validation(moment_results)

============================================================

Moment Validation: Distribution

============================================================

X_mean : sample = 1.3374, theory = 1.3497, rel_err = 9.18e-03

Y_mean : sample = 2.7129, theory = 2.6995, rel_err = 4.98e-03

X_var : sample = 3.8364, theory = 3.8272, rel_err = 2.43e-03

Y_var : sample = 4.5105, theory = 4.5107, rel_err = 5.71e-05

1.2 MLE Fitting (Complete Data)

[5]:

# Test MLE fitting for joint distribution

fitted_dist, fitted_params, param_errors = test_joint_fitting(

JointGeneralizedHyperbolic,

params_1d,

n_samples=10000,

random_state=42

)

print_fitting_results(params_1d, fitted_params, param_errors, name="JointGH")

============================================================

Fitting Results: JointGH

============================================================

Parameter True Fitted Rel.Error

------------------------------------------------------------

mu 0.0000 -0.0110 1.10e+08

gamma 0.5000 0.5025 5.00e-03

sigma 1.0000 1.0071 7.11e-03

p 1.0000 0.9702 2.98e-02

a 1.0000 0.9982 1.76e-03

b 1.0000 1.0471 4.71e-02

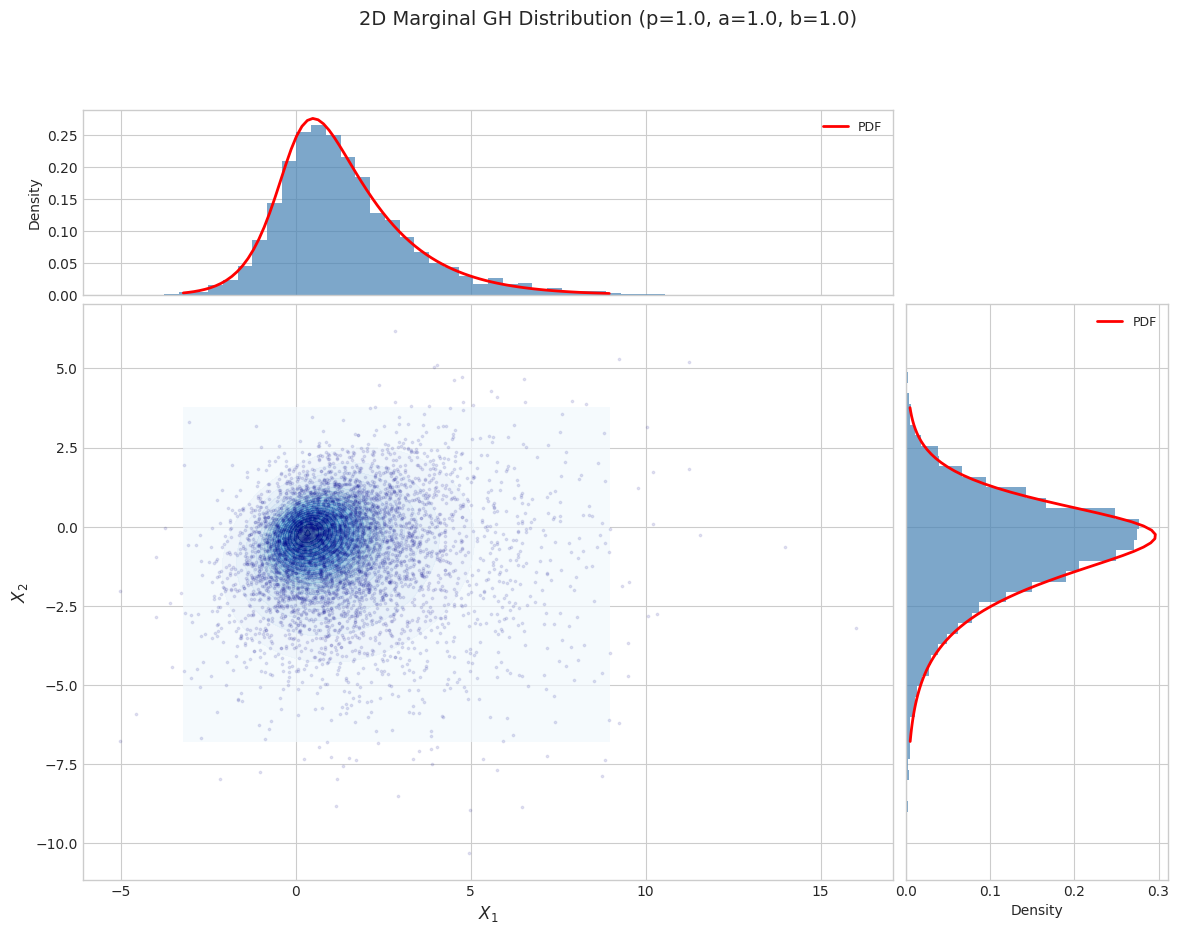

2. Marginal Distribution: \(f(x)\) (2D Case)

The marginal distribution is NOT an exponential family.

[6]:

# Define 2D marginal distribution parameters

params_2d = {

'mu': np.array([0.0, 0.0]),

'gamma': np.array([0.5, -0.3]),

'sigma': np.array([[1.0, 0.3], [0.3, 1.0]]),

'p': 1.0,

'a': 1.0,

'b': 1.0

}

# Create marginal distribution

gh_2d = GeneralizedHyperbolic.from_classical_params(**params_2d)

print("Created:", gh_2d)

Created: GeneralizedHyperbolic(d=2, p=1.000, a=1.000, b=1.000)

[7]:

# Visualize 2D marginal distribution

fig = plot_marginal_distribution_2d(

gh_2d, n_samples=5000, random_state=42,

title=f"2D Marginal GH Distribution (p={params_2d['p']}, a={params_2d['a']}, b={params_2d['b']})"

)

plt.tight_layout()

plt.show()

/tmp/ipykernel_2346057/2887610028.py:6: UserWarning: This figure includes Axes that are not compatible with tight_layout, so results might be incorrect.

plt.tight_layout()

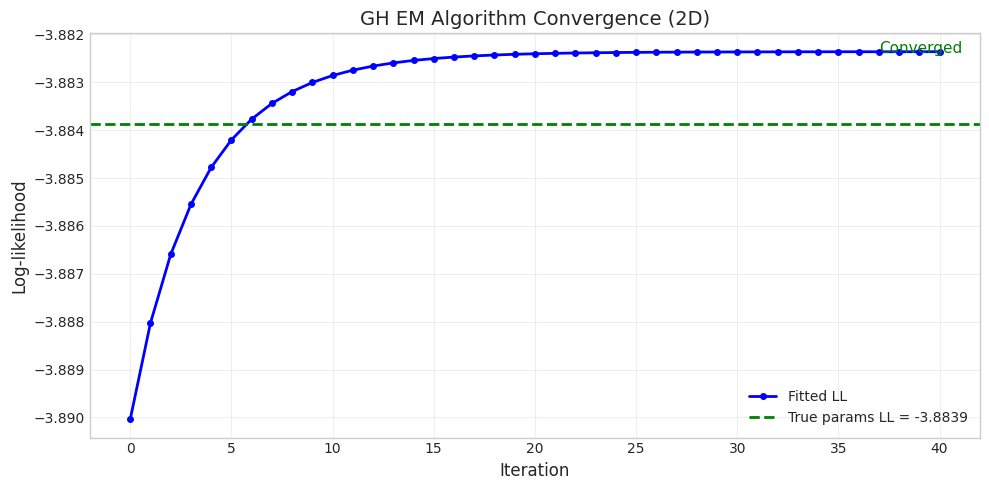

2.1 EM Algorithm Fitting

The marginal distribution requires the EM algorithm for fitting.

[17]:

# Generate data from true distribution

true_gh = GeneralizedHyperbolic.from_classical_params(**params_2d)

X_data = true_gh.rvs(size=5000, random_state=42)

# Compute true log-likelihood for reference

true_ll = np.mean(true_gh.logpdf(X_data))

print(f"True parameters log-likelihood: {true_ll:.4f}")

# Fit using EM algorithm with regularization

print("\nFitting with EM algorithm (det_sigma_one regularization)...")

fitted_gh, convergence = fit_and_track_convergence(

GeneralizedHyperbolic,

X_data,

max_iter=100,

tol=1e-2, # Use reasonable tolerance for GH

regularization='det_sigma_one',

)

print(f"\nConverged: {convergence.converged}")

print(f"Final log-likelihood: {convergence.log_likelihoods[-1]:.4f}")

print(f"Improvement over true: {convergence.log_likelihoods[-1] - true_ll:.4f}")

True parameters log-likelihood: -3.8839

Fitting with EM algorithm (det_sigma_one regularization)...

Converged: True

Final log-likelihood: -3.8824

Improvement over true: 0.0015

[18]:

# Plot convergence with true log-likelihood reference

fig = plot_em_convergence(

convergence,

title="GH EM Algorithm Convergence (2D)",

true_ll=true_ll

)

plt.show()

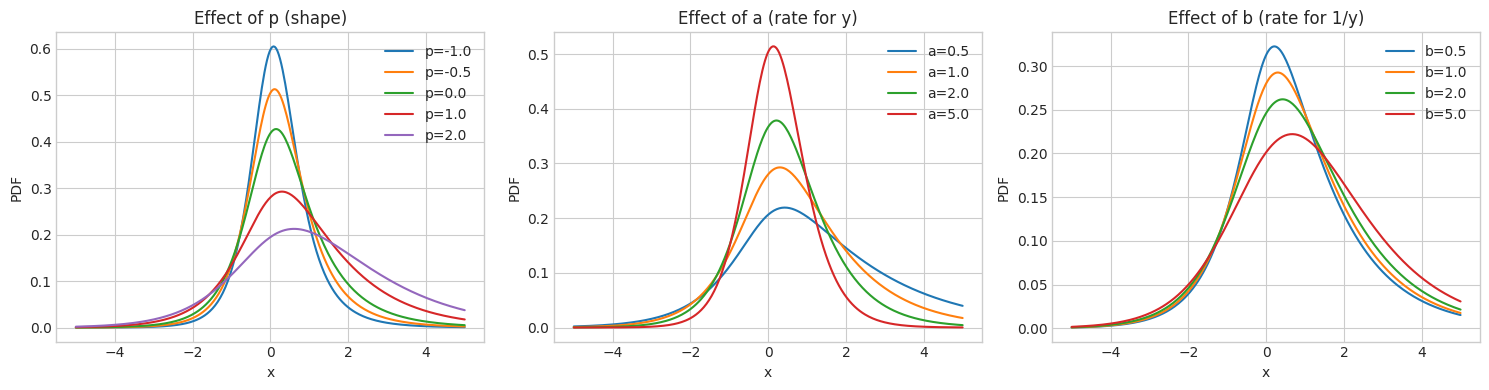

3. Effect of GIG Parameters

The GIG parameters \((p, a, b)\) control the shape of the mixing distribution and thus the behavior of the GH distribution.

[10]:

fig, axes = plt.subplots(1, 3, figsize=(15, 4))

# Base parameters

base_mu = np.array([0.0])

base_gamma = np.array([0.3])

base_sigma = np.array([[1.0]])

x = np.linspace(-5, 5, 300)

# Effect of p

ax = axes[0]

for p in [-1.0, -0.5, 0.0, 1.0, 2.0]:

try:

gh = GeneralizedHyperbolic.from_classical_params(

mu=base_mu, gamma=base_gamma, sigma=base_sigma, p=p, a=1.0, b=1.0

)

pdf = np.array([gh.pdf(np.array([xi])) for xi in x])

ax.plot(x, pdf, label=f'p={p}')

except:

pass

ax.set_title('Effect of p (shape)')

ax.set_xlabel('x')

ax.set_ylabel('PDF')

ax.legend()

# Effect of a

ax = axes[1]

for a in [0.5, 1.0, 2.0, 5.0]:

try:

gh = GeneralizedHyperbolic.from_classical_params(

mu=base_mu, gamma=base_gamma, sigma=base_sigma, p=1.0, a=a, b=1.0

)

pdf = np.array([gh.pdf(np.array([xi])) for xi in x])

ax.plot(x, pdf, label=f'a={a}')

except:

pass

ax.set_title('Effect of a (rate for y)')

ax.set_xlabel('x')

ax.set_ylabel('PDF')

ax.legend()

# Effect of b

ax = axes[2]

for b in [0.5, 1.0, 2.0, 5.0]:

try:

gh = GeneralizedHyperbolic.from_classical_params(

mu=base_mu, gamma=base_gamma, sigma=base_sigma, p=1.0, a=1.0, b=b

)

pdf = np.array([gh.pdf(np.array([xi])) for xi in x])

ax.plot(x, pdf, label=f'b={b}')

except:

pass

ax.set_title('Effect of b (rate for 1/y)')

ax.set_xlabel('x')

ax.set_ylabel('PDF')

ax.legend()

plt.tight_layout()

plt.show()

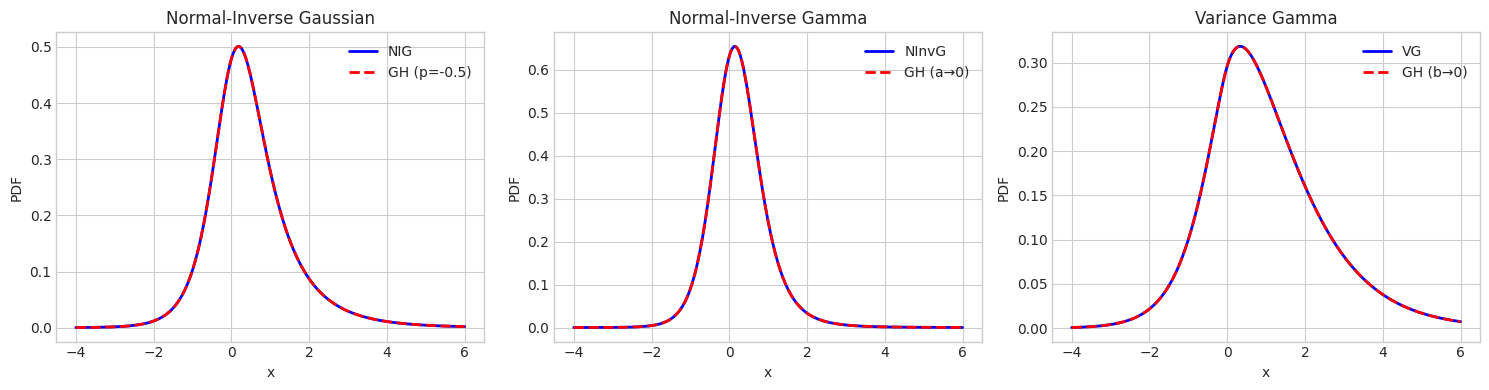

4. Special Case Comparison

Verify that GH special cases match their dedicated implementations.

[11]:

# Test parameters

mu = np.array([0.0])

gamma = np.array([0.5])

sigma = np.array([[1.0]])

x = np.linspace(-4, 6, 300)

fig, axes = plt.subplots(1, 3, figsize=(15, 4))

# NIG comparison (p = -0.5)

ax = axes[0]

nig_params = {'delta': 1.0, 'eta': 1.0}

nig = NormalInverseGaussian.from_classical_params(mu=mu, gamma=gamma, sigma=sigma, **nig_params)

gh_nig = GeneralizedHyperbolic.as_normal_inverse_gaussian(mu=mu, gamma=gamma, sigma=sigma, **nig_params)

nig_pdf = np.array([nig.pdf(np.array([xi])) for xi in x])

gh_nig_pdf = np.array([gh_nig.pdf(np.array([xi])) for xi in x])

ax.plot(x, nig_pdf, 'b-', linewidth=2, label='NIG')

ax.plot(x, gh_nig_pdf, 'r--', linewidth=2, label='GH (p=-0.5)')

ax.set_title('Normal-Inverse Gaussian')

ax.set_xlabel('x')

ax.set_ylabel('PDF')

ax.legend()

print(f"NIG mean: {nig.mean()}, GH mean: {gh_nig.mean()}")

# NInvG comparison (a → 0)

ax = axes[1]

ninvg_params = {'shape': 3.0, 'rate': 1.0}

ninvg = NormalInverseGamma.from_classical_params(mu=mu, gamma=gamma, sigma=sigma, **ninvg_params)

gh_ninvg = GeneralizedHyperbolic.as_normal_inverse_gamma(mu=mu, gamma=gamma, sigma=sigma, **ninvg_params)

ninvg_pdf = np.array([ninvg.pdf(np.array([xi])) for xi in x])

gh_ninvg_pdf = np.array([gh_ninvg.pdf(np.array([xi])) for xi in x])

ax.plot(x, ninvg_pdf, 'b-', linewidth=2, label='NInvG')

ax.plot(x, gh_ninvg_pdf, 'r--', linewidth=2, label='GH (a→0)')

ax.set_title('Normal-Inverse Gamma')

ax.set_xlabel('x')

ax.set_ylabel('PDF')

ax.legend()

print(f"NInvG mean: {ninvg.mean()}, GH mean: {gh_ninvg.mean()}")

# VG comparison (b → 0)

ax = axes[2]

vg_params = {'shape': 2.0, 'rate': 1.0}

vg = VarianceGamma.from_classical_params(mu=mu, gamma=gamma, sigma=sigma, **vg_params)

gh_vg = GeneralizedHyperbolic.as_variance_gamma(mu=mu, gamma=gamma, sigma=sigma, **vg_params)

vg_pdf = np.array([vg.pdf(np.array([xi])) for xi in x])

gh_vg_pdf = np.array([gh_vg.pdf(np.array([xi])) for xi in x])

ax.plot(x, vg_pdf, 'b-', linewidth=2, label='VG')

ax.plot(x, gh_vg_pdf, 'r--', linewidth=2, label='GH (b→0)')

ax.set_title('Variance Gamma')

ax.set_xlabel('x')

ax.set_ylabel('PDF')

ax.legend()

print(f"VG mean: {vg.mean()}, GH mean: {gh_vg.mean()}")

plt.tight_layout()

plt.show()

NIG mean: [0.5], GH mean: [0.5]

NInvG mean: [0.25], GH mean: [0.25]

VG mean: [1.], GH mean: [1.]

5. Parameter Regularization

The GH model is not identifiable since \((\mu, \gamma/c, \Sigma/c, p, cb, a/c)\) gives the same distribution for any \(c > 0\).

Available regularization methods:

det_sigma_one: Fix \(|\Sigma| = 1\) (recommended)sigma_diagonal_one: Fix \(\Sigma_{11} = 1\)fix_p: Fix \(p\) to a specific valuenone: No regularization

[12]:

from normix.distributions.mixtures import REGULARIZATION_METHODS

print("Available regularization methods:")

for name in REGULARIZATION_METHODS:

print(f" - {name}")

Available regularization methods:

- det_sigma_one

- sigma_diagonal_one

- fix_p

- none

[13]:

# Compare different regularizations

X_data = true_gh.rvs(size=3000, random_state=42)

regularizations = ['det_sigma_one', 'fix_p']

results = {}

for reg in regularizations:

print(f"\n--- Regularization: {reg} ---")

fitted = GeneralizedHyperbolic()

kwargs = {'regularization': reg}

if reg == 'fix_p':

kwargs['regularization_params'] = {'p_fixed': 1.0}

fitted.fit(X_data, max_iter=30, verbose=0, **kwargs)

params = fitted.classical_params

print(f" p = {params.p:.4f}")

print(f" a = {params.a:.4f}")

print(f" b = {params.b:.4f}")

print(f" |Σ| = {np.linalg.det(params.sigma):.4f}")

print(f" Mean = {fitted.mean()}")

results[reg] = fitted

--- Regularization: det_sigma_one ---

p = 0.5896

a = 0.9347

b = 1.6064

|Σ| = 1.0000

Mean = [ 1.27654667 -0.82581383]

--- Regularization: fix_p ---

p = 1.0000

a = 0.3575

b = 14.3831

|Σ| = 0.0738

Mean = [ 1.58034717 -1.01797886]

6. Exponential Family Structure

The joint distribution is an exponential family with:

Sufficient statistics:

Natural parameters:

[15]:

# Show parameter conversions

print("=== Exponential Family Parameters ===")

print(f"\nClassical: {jgh_1d.classical_params}")

print(f"\nNatural: {jgh_1d.natural_params}")

print(f"\nExpectation: {jgh_1d.expectation_params[:6]}...") # First 6 components

=== Exponential Family Parameters ===

Classical: GHParams(mu=array([0.]), gamma=array([0.5]), sigma=array([[1.]]), p=np.float64(1.0), a=np.float64(1.0), b=np.float64(1.0))

Natural: [-0.5 -1. -1.125 0.5 0. -0.5 ]

Expectation: [0.69948394 0.69948394 2.69948394 1.34974197 0.5 1.67487098]...

[16]:

# Verify sufficient statistics match expectation parameters

n_samples = 20000

X, Y = jgh_1d.rvs(size=n_samples, random_state=42)

t_samples = jgh_1d._sufficient_statistics(X, Y)

eta_sample = np.mean(t_samples, axis=0)

eta_theory = jgh_1d.expectation_params

print("E[t(X,Y)] from samples vs theoretical:")

print(f" E[log Y]: {eta_sample[0]:.4f} vs {eta_theory[0]:.4f}")

print(f" E[1/Y]: {eta_sample[1]:.4f} vs {eta_theory[1]:.4f}")

print(f" E[Y]: {eta_sample[2]:.4f} vs {eta_theory[2]:.4f}")

E[t(X,Y)] from samples vs theoretical:

E[log Y]: 0.7052 vs 0.6995

E[1/Y]: 0.6942 vs 0.6995

E[Y]: 2.7129 vs 2.6995

Summary

The Generalized Hyperbolic distribution:

Most general normal variance-mean mixture

Joint distribution is an exponential family

Marginal distribution requires EM algorithm for fitting

Special cases include VG, NIG, NInvG, and more

Regularization is needed due to identifiability issues